Mobile Payments: Supporting Europe’s Move to a Cashless Society

KEY POINTS

- In 2015, only 3% of in-store payments in Europe were conducted by mobile phones, according to market data firm GfK.

- Western Europe has the highest smartphone penetration globally, and it has the necessary infrastructure to support the use of digital money.

- In 2016, more than 20% of Visa’s face-to-face transactions in Europe will be contactless payments, according to Visa Europe.

- By 2020, all point-of-sale (POS) terminals in Europe will be able to accept mobile payments, according to Visa Europe and MasterCard.

In a number of European countries, consumers have rapidly adopted contactless payments. Some banks, retailers and transportation companies have already gone completely cashless, no longer accepting cash at their branches or at the POS. In many countries, making face-to-face payments using a smartphone instead of a card is the next step in the path to a near-cashless society.

In this report, we look at the scale and development of mobile payments, with a focus on face-to-face payment options such as Apple Pay and Android Pay. We consider the global context in terms of number of users and infrastructure in major regions, before turning to Europe as an example of a Western market that is leading in the adoption of new payment technologies.

MOBILE PAYMENTS VS. MOBILE POS

MOBILE PAYMENTS VS. MOBILE POS

Mobile phones have become an increasingly common tool for making in-store payments, for banking and for buying online. The term “mobile payment” covers all transactions—including peer-to-peer (P2P) transactions, bill payments and ordering items from an e-commerce site—made using any type of mobile phone. “Mobile POS,” on the other hand, refers to face-to-face payments made using a smartphone or tablet wherein the user pays for a product or service on the spot.

Essentially, mobile payment methods are differentiated according to the mobile phone’s ability to work with different types of technologies:

- Short message service (SMS) payments, such as those enabled by M-Pesa in Africa, can be made using any mobile phone.

- Wireless application protocol (WAP) payments include those made via PayPal as well as QR code payments such as those made through the Starbucks barcode-scanning payment app. These can be made using any smartphone.

- Near-field communication (NFC) payments, such as those made via Apple Pay and Samsung Pay, can be made only with smartphones that enable the technology.

Mobile P2P money transfers and mobile bill payments are already established payment methods globally, whereas mobile face-to-face payments are still growing in terms of adoption, and so will see further developments, according to consulting firm Ernst & Young.

The European Central Bank (ECB) considers NFC-based mobile payments among the most promising payment methods for consumers. Suppliers are making consistent investments to update their NFC hardware and merchants are installing contactless points of interaction based on NFC technology.

NFC payments are expected to increase as more consumers adopt the technology. Management consulting company Arthur D. Little estimates that global NFC-enabled smartphone penetration will increase from 23% in 2014 to 72% in 2018.

MOBILE PAYMENTS ACROSS THE GLOBE: ASIA-PACIFIC REGION STILL LEADING

According to GfK’s FutureBuy 2015 study, only 3% of in-store payments in Europe were conducted by mobile phone in 2015. In the US, mobile payments also accounted for 3% of total in-store payments last year, compared to 9% in countries in the Asia-Pacific region, which led globally in terms of mobile payment usage.

Europeans may not be the most active users of mobile payments worldwide, but adoption of contactless payments—which include contactless card payments—has been rapid in Europe. Face-to-face mobile payment services such as Apple Pay are effectively a subset of contactless payments. And face-to-face contactless transactions processed by Visa in Europe have increased significantly. According to Visa Europe:

- In 2013, one in 60 face-to-face payments were made using contactless payment services.

- Between May 1, 2015, and April 30, 2016, however, contactless payments represented more than one in five of Visa Europe’s face-to-face payments. The growth and popularity of contactless payments have been driven by “everyday spend,” such as spending on lunch, restaurants and groceries, and by more merchants incorporating contactless payments into their offerings.

In our September 2015 report The Changing Face of Mobile Payments, we discussed the popularity of mobile payments in China, where Alipay Wallet and WeChat Wallet have introduced user-friendly and widely popular mobile payment services.

So, how do other regions measure up versus the Asia-Pacific region?

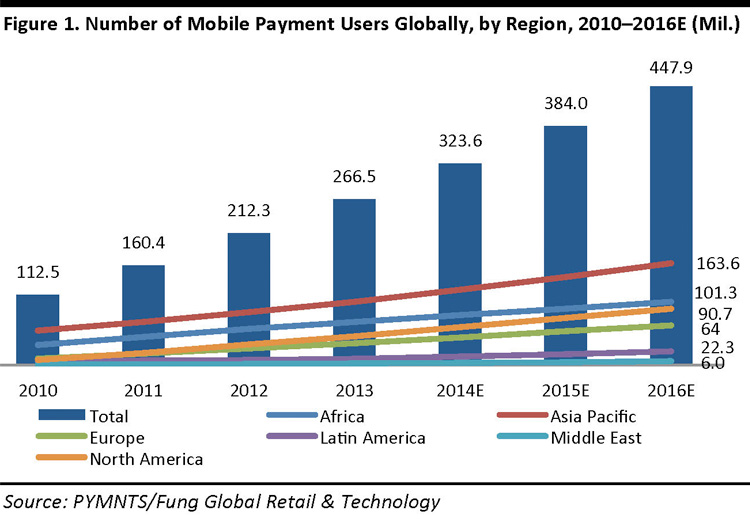

Payments and commerce analytics company PYMNTS estimates that the Asia-Pacific region will continue to lead in terms of number of mobile payment users in 2016, followed by Africa, the US and Europe. The firm expects the number of mobile payment users worldwide to grow by 16.6%, to 447.9 million, in 2016.

There are two things that should be noted about the figures from PYMNTS: First, the Asia-Pacific region and Africa have significantly bigger populations than the US and Europe do. Second, PYMNTS includes all mobile payment methods, including SMS payments, in its figures—the numbers are not simply for face-to-face retail transactions such as those made through Apple Pay.

The high number of mobile payment users in Africa can be explained by the popularity of SMS payment systems across the continent; these include M-Pesa, which was launched by Vodafone and Safaricom in Kenya in 2007. With M-Pesa, mobile phone users can transfer money and pay for products and services by sending PIN-secured text messages. According to the World Bank’s Global Findex Database report, in 2014, 12% of adults living in Sub-Saharan African countries had a mobile money account, compared to 2% worldwide. However, in Africa, the infrastructure needed to enable digital mobile payments (such as Apple Pay payments) lags that of other developing regions.

HIGH DIGITAL MONEY READINESS IN WESTERN EUROPE

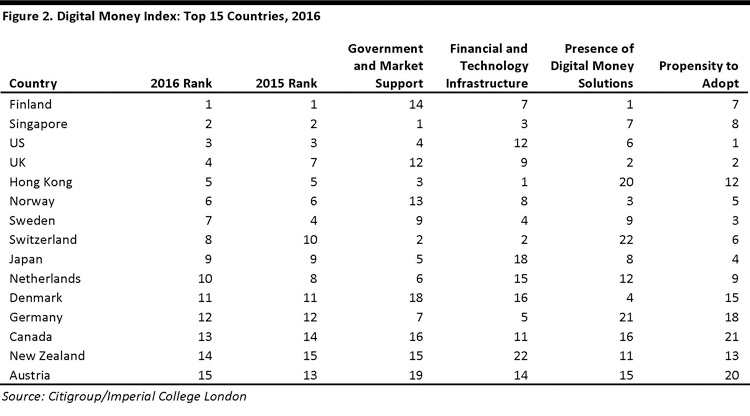

Developed by Citigroup and Imperial College London, the Digital Money Index measures 90 countries’ digital money readiness, and how they are adapting to the migration from cash to digital payments. Nine out of 15 top-ranked digital-ready countries measured by the index are European, with Finland leading, followed by Singapore and the US.

Citigroup notes that progress in adopting digital money in materially ready and mature digital countries is largely a consequence of investments in next-generation mobile broadband infrastructure and high smartphone penetration levels.

IN CONTEXT: SMARTPHONE OWNERSHIP AND BANK ACCOUNT UPTAKE

There are two fundamental prerequisites that consumers must meet in order to make mobile payments: they must have both a smartphone and a bank account. Below, we take a look at how penetration rates for these two items vary by region.

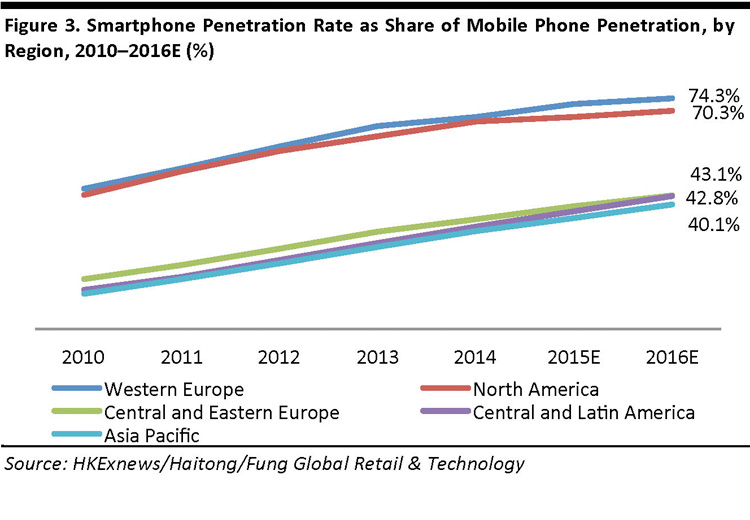

Smartphone Penetration Lags in Eastern Europe, Latin America and the Asia-Pacific Region

There are two tiers of smartphone penetration rates across the globe:

- North America and Western Europe lead by a clear margin in terms of smartphone ownership, and so comprise the top tier of regions. HKExnews and Haitong estimate that 70.3% of mobile phone owners in North America and 74.3% of mobile phone owners in Western Europe currently have a smartphone.

- Central and Eastern Europe, Central and Latin America, and the Asia-Pacific region comprise the second tier. It is estimated that even by 2019, only about half of mobile phone users in each of these three regions will be using a smartphone.

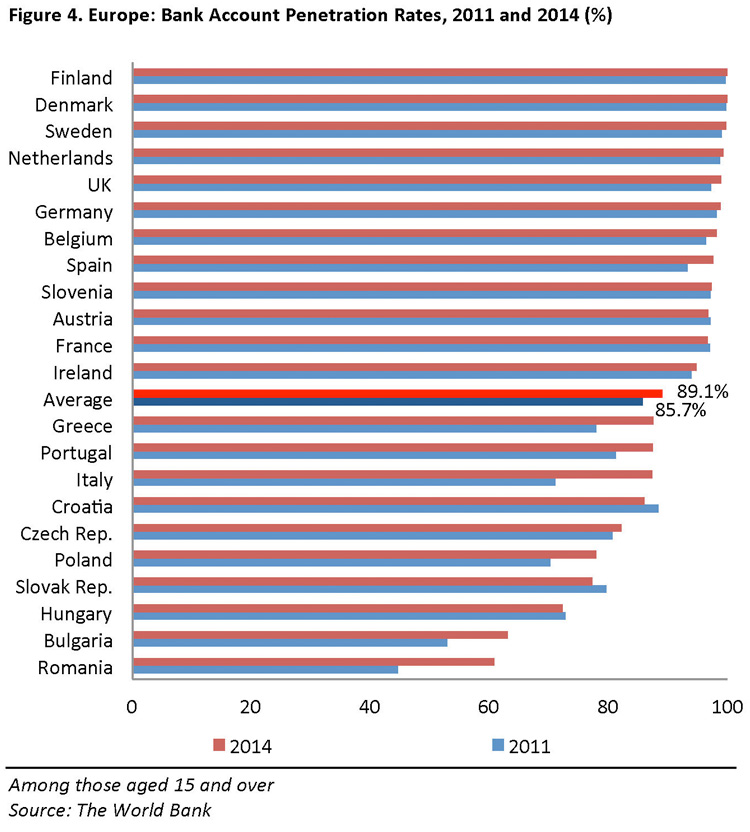

Bank Account Penetration Still Relatively Low in Eastern Europe

Bank account penetration is extremely high in Western Europe. In 2014, 100% of the population age 15 and over in Finland and Denmark had a bank account, according to the World Bank. In comparison, only 60.8% of the population in Romania and 63% of the population in Bulgaria had a bank account in 2014.

IN FOCUS: EUROPE’S MOVE TO A CASHLESS SOCIETY

The metrics charted above show that Western Europe is leading in terms of adopting new payment methods, including mobile payments: countries in this region take leading positions in the Digital Money Index, their smartphone ownership rates are among the highest in the world, and their bank account penetration rates also tend to be high. So, it is worthwhile to focus on the region to see where consumer payments may be heading.

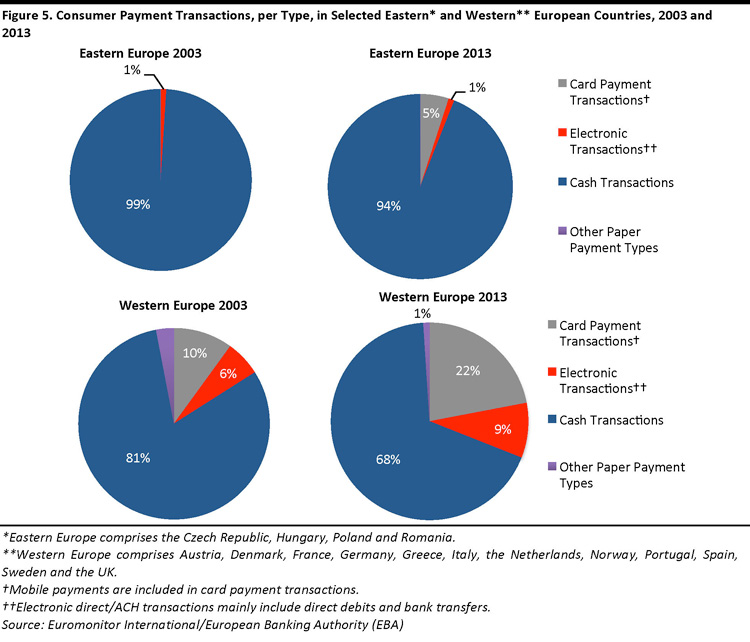

Is Western Europe heading toward a cashless future? Perhaps, in the coming decades, but not quite yet. Despite the developments in digital payment methods, cash is still commonly used in many regions, particularly in Eastern Europe. According to Euromonitor International, cash transactions accounted for 68% of all consumer payment transactions in Western Europe in 2013 (latest available). But cash’s share was down 13 percentage points in a decade, and the cash payments figure for Western Europe was notably lower than the 94% figure for Eastern Europe.

According to the EBA, cash payments in Western Europe are expected to continue to decline as card payments and NFC payments grow share.

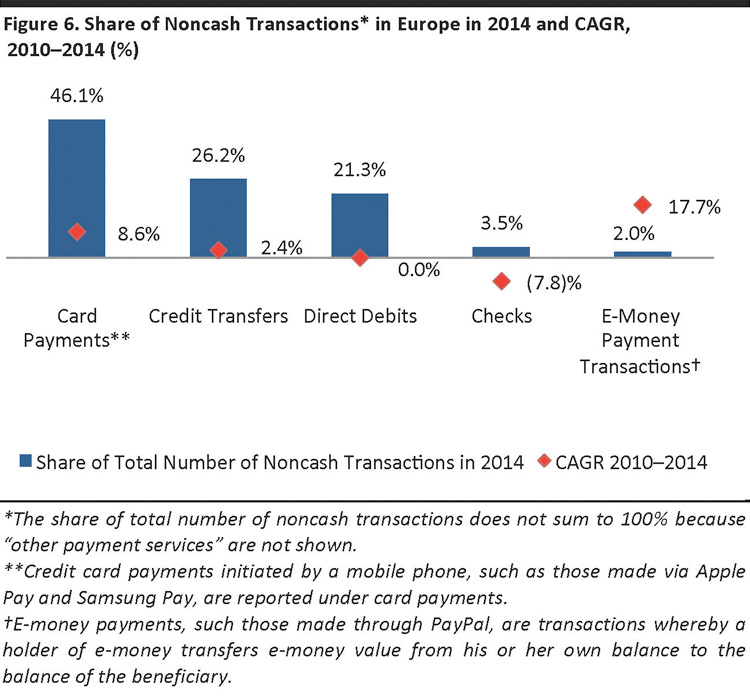

Strong Growth in E-Money Payment Transactions in Europe

The ECB offers a more detailed breakdown of noncash transactions in Europe, showing that card payments and e-money payment transactions have grown the fastest in recent years. Card payments, which grew at a CAGR of 8.6% in the four years ended 2014, include mobile payments such as those made through Apple Pay and Android Pay. These are tied to a stored debit card. E-money transactions, which grew at a CAGR of 17.7% in the same four years, include those made through services such as PayPal, which are intermediaries and can “store” payments.

High Payment Card and Contactless Payment Usage in the UK

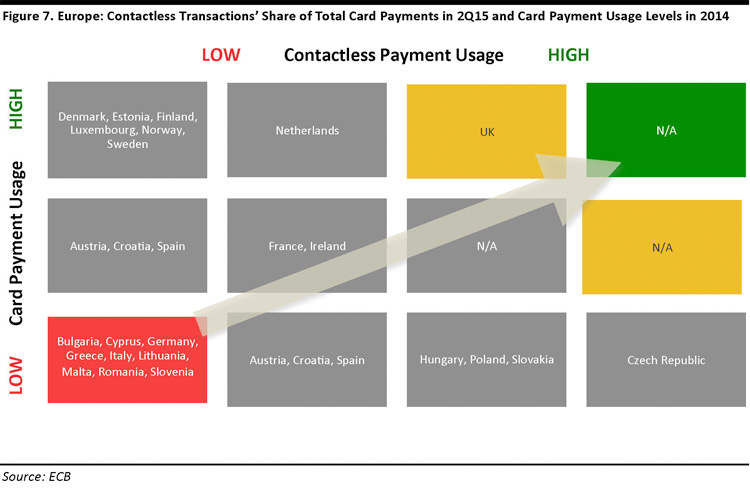

Contactless payments in many markets are dominated by contactless debit and credit cards. Data on contactless payment penetration, shown below, does not split out mobile contactless payments from card-based contactless payments.

The graphic below brings together ECB data on levels of card payment transactions and the share of face-to-face card payments that are contactless. The number of card transactions per capita is defined as follows:

- Low: <75 transactions per year

- Medium: 75–150 transactions per year

- High: >150 transactions per year

Contactless payment penetration levels are plotted across rows from left to right, ranging from those that account for less than 3% of the total number of face-to-face card transactions to those that account for more than 50%.

These data indicate that no countries have yet hit the sweet spot of high contactless payment usage and high card payment usage (indicated by the top right box in the graphic)—although the UK comes the closest.

Eastern European countries score highly in terms of contactless payments as a percent of all face-to-face card transactions. However, card payment usage in many of these countries is still rather low. In the Czech Republic, for example, over 50% of face-to-face card transactions were made using contactless payments in the second quarter of 2015, but card payment usage in 2014 was low, at an average of about 1.5 transactions per person per week.

The UK scores highly in both contactless and card payments (with an average of more than three transactions per person per week). Overall, Western European countries rank highly in payment card usage, but contactless payment usage is still not widespread.

The ECB notes that countries with high contactless payment usage, such as the UK, Poland and the Czech Republic, have successfully coordinated point-of-interest terminals in consumer-centric grocery and transportation sectors.

From Contactless Payments to Mobile Payments

One counterpoint to the presumed relationship between contactless payments and mobile payments is the US (not shown in the data above). Anecdotal evidence suggests that mobile payments have had greater consumer impact in the US because they are a relatively new offering in the country and offer a double added convenience: the novelty of contactless payment plus the convenience of using a smartphone to pay. In countries such as the UK, where contactless payment options are already commonplace, the enhanced convenience that mobile payment options offer to consumers is less substantial.

According to the ECB, it is easier and simpler to introduce contactless cards than it is to introduce mobile contactless payments, as contactless cards involve the same stakeholders as in the traditional contact card ecosystem. The mobile ecosystem is highly competitive and mobile payment services are built up by many different parties and components, such as mobile network operators, payment processors and NFC-enabled devices.

EUROPEAN COUNTRY SNAPSHOTS

UK

British mobile users have been among the earliest European adopters of contactless payments. From 2015 to 2016, the country jumped three places, to fourth place, on the Digital Money Index. According to MasterCard, transportation has been a key driver of contactless payment adoption by consumers in the UK:

- Transport for London (TfL) reports that more than 300 million journeys have been made using contactless payments since the method was first accepted on London buses in September 2012. The technology was expanded to cover the majority of London’s transportation in September 2014. TfL’s buses went cashless in 2014, accepting only contactless payment methods. Mobile devices accounted for approximately 3.5% of all TfL contactless journeys in January 2016, and that share is expected to increase further throughout the year.

Visa Europe estimates that 25% of Brits will use mobile payments on a daily basis by 2020, up from 8% in 2015. The company also reported 237% year-over-year growth in contactless payments in the UK in the six months ended March 2015. This was largely due to a September 2015 increase in the maximum pay limit, from £20 (US$31) to £30 (US$46). Restaurants were among the businesses benefiting the most; they saw a 155% increase in contactless payments during the period.

Germany

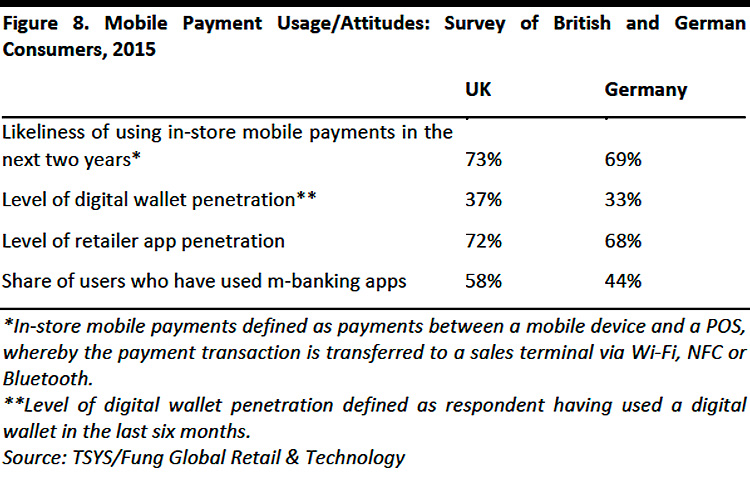

While many Germans still prefer to use cash to pay for everyday items, mobile payments are expected to gain ground. Payment service company TSYS surveyed British and German consumers in 2015 to understand regional differences in payment preferences. The survey indicated that German consumers are less experienced than British consumers are in using digital wallets, such as Apple Wallet, that store card-payment details. However, almost as many Germans as Brits believe they will be using in-store mobile payments in coming years.

The Netherlands

MasterCard conducted a pilot of its biometric payment system in the Netherlands, and reports that 83% of users in the country think biometric identity checks provide more security than passwords do, and that 93% think biometric checks are more convenient than passwords.

Some Dutch banks, including Rabobank and ING, have introduced their own mobile payment services in their home market using NFC technology.

Spain

In 2012, Spanish banking group CaixaBank, in partnership with Visa Europe, made Barcelona the first major city in Europe to extensively use contactless payment technology. The bank distributed more than 1 million contactless cards in the first year of the program, and enabled customers to make contactless payments using their smartphones beginning in 2014.

In June 2016, Samsung launched its Samsung Pay service in Spain, the first European country where the company introduced the offering.

Sweden

Sweden could become the first cashless country in the world. According to a study by Stockholm’s KTH Royal Institute of Technology, Sweden could become a cashless society by 2030. Several leading banks have already completely digitalized their branches and no longer accept cash. The Riksbank, Sweden’s central bank, notes that, in 2014, cash in circulation as a share of GDP was 2.0%, compared to 3.0% in Denmark and 3.5% in the UK; some analysts estimate this ratio could drop to 0.5% in Sweden by 2020.

The Czech Republic

As noted above, contactless penetration in the Czech Republic is very high. According to Visa Europe, contactless payments (mainly made through contactless payment cards) accounted for nearly 60% of in-store payments in the country in 2015. Yet cards are used infrequently in the Czech Republic, relative to some other European countries: the average number of electronic transactions per Czech household annually is only 70, compared to more than 300 in Scandinavia.

OUTLOOK: MOBILE PAYMENTS WIDELY AVAILABLE IN EUROPE BY 2020

While payment cards are widely used in Europe, contactless mobile payments are not as popular—as noted earlier, only 3% of in-store payments in Europe were conducted via mobile phone in 2015. Despite the current low mobile payment penetration in Europe, payment system providers are rapidly introducing the infrastructure and secured systems needed to enable mobile payments.

Visa Europe, which is the leading payments system in Europe, with a 57.5% market share in 2015, believes that all Visa POS terminals in Europe will accept contactless NFC payments by 2020.

MasterCard believes that high-value mobile payments will be available across Europe by 2017, thanks to upgrades of contactless payment terminals. Currently, the maximum limit for contactless payments in the UK is £30 (US$46); in many other European countries, it is €25 (US$27). MasterCard also believes contactless payments will be available at all its POS terminals in Europe by 2020.

The company has invested in biometric payment systems, which allow customers to pay online after their identity is verified via fingerprint or facial recognition (via a selfie photo). International Card Services conducted the first successful biometric payment pilot in the Netherlands in 2015, and the company is planning to launch this payment technology in other parts of Europe and in the US and Canada in the summer of 2016.

Visa and MasterCard have both partnered with Apple Pay and Android Pay to develop mobile payment services using Apple and Android devices, and to introduce mobile payments in new regions.

KEY TAKEAWAYS: MUCH POTENTIAL FOR MOBILE PAYMENTS IN EUROPE

Western Europe has tended to lead other regions on the metrics that support mobile payments. In order to make mobile payments, consumers must have both a smartphone and a bank account, and the region ranks the highest globally in terms of numbers of smartphone users and bank account holders, with averages above 95%. Yet, even in Europe, only a small number of face-to-face payments are currently made using mobile devices—such transactions accounted for just 3% of all POS payments in 2015.

Mobile payment adoption in Europe is expected to make great leaps in the coming years. Leading payment operators expect that all payment terminals in Europe will be NFC ready by 2020. Consumer sectors that see a high number of low-value transactions channeled through payment terminals (such as transportation and grocery retail) look to offer the greatest opportunities; because consumers make frequent purchases in these categories, they desire speed and convenience in such transactions. These sectors can serve to introduce mobile payments to consumers, who will likely want to use them in other sectors once they are familiar with how they work.

Some Western European countries are on the path to becoming near-cashless societies, and mobile face-to-face payments are likely to play a significant role in this shift.